Apr 28, 2020 | HR, Management

Declines in consumer confidence and decreased sales can threaten all businesses, but small businesses can be particularly vulnerable. They often don’t have reserves to help them weather difficult times. From protecting your cash flow to building your customer base, implementing a few practices in advance can help recession-proof your business so it survives and even thrives during economic downturns.

Protect Your Cash Flow

Cash flow is the lifeblood of your business. Money must continue inflowing and outflowing for optimum business health, with the obvious goal being that you bring in more income than you must spend on expenses. You’ll have expenses as long as your business exists.

Note: Admittedly, it can be hard to keep the cash flowing in. Recession-proof your business by implementing strategies to keep the cash flow moving, from increasing sales or billable services to trimming unnecessary expenses.

Review Inventory Management

See if anything can be done to reduce your inventory costs without sacrificing the quality of goods sold or inconveniencing your customers. Maybe you’re ordering too many of particular items, or something can be sourced somewhere else at a better price. Is there a drop-shipping alternative that will work for you so you can eliminate shipping and warehousing costs?

Note: Just because you’ve always ordered something from a particular supplier or done things in a particular way doesn’t mean that you have to keep doing things that way, especially when other ways can save you money.

Focus on Core Competencies

Small business owners often simplify the concept of “diversification,” translating it to simply “different.”

Simply adding other products or services to your offerings isn’t diversification. At best, it’s a waste of time and money. Worse, it can damage your core business by taking your time and your money away from what you do best, damaging your brand and reputation.

Note: Drop the extras and focus on what you do best that’s most profitable.

Win the Competition’s Customers

You must continue to expand your customer/client base if your small business is going to prosper in tough times. This means drawing customers from your competition.

Offer something more or different than what the other guy does. Research your competition and see what you can do to entice their customers into becoming your customers. How are your competitors advertising? Visit their business locations. Ask consumers what they like or don’t like about those companies, then tweak your own business practices accordingly.

Make the Most of Current Customers

We’ve all heard the old adage that a bird in the hand is worth two in the bush. The bird in the hand is your customer or client, and they’re an opportunity to make more sales without incurring the costs of finding new customers.

Even better, they might be loyal customers, giving you many more sales opportunities. You can’t afford to ignore the potential profits of shifting your sales focus to include established customers if you want to recession-proof your business.

The key here is excellent customer service. Ensure that your customers or clients love what you do or sell, and keep them happy. Yes, that means the customer is always right. Identify their needs, then meet them. You want to retain their business all costs. This is more important during a recession than at any other time.2

Don’t Cut Back on Marketing

Many small businesses make the mistake of cutting their marketing budget to the bone in lean times, or even eliminating it entirely, but this is exactly when your small business needs marketing the most.

Consumers are restless. They’re always looking to make changes in their buying decisions. Help them find your products and services and to choose them rather than others by getting your name out there. Don’t quit marketing. Step up your marketing efforts.

Watch Your Credit Scores

Hard times make it harder to borrow, and small business loans are often among the first to feel the squeeze, particularly for businesses with iffy credit ratings. Monitor yours frequently and keep on top of them. There are three major business credit bureaus and each assesses your business’s creditworthiness differently:

– Experian

– Equifax

– Dunn & Bradstreet3

Note: Keep tabs on your personal credit rating as well and do whatever is necessary to keep both in good shape.

You’ll stand a much better chance of being able to borrow the money you need to keep your business afloat if you have good personal credit as well. And keep in mind that the U.S. Small Business Administration makes easy-qualifying loans available during times of national economic crisis, in addition to its usual funding programs.

The Bottom Line

Nothing will make your small business 100% recession-proof, but implementing these can help ensure that your business survives tough times and possibly even profits from them. It all begins with analyzing how you’re doing things now and looking for ways to improve.

Source: The Balance

Apr 28, 2020 | HR, Management

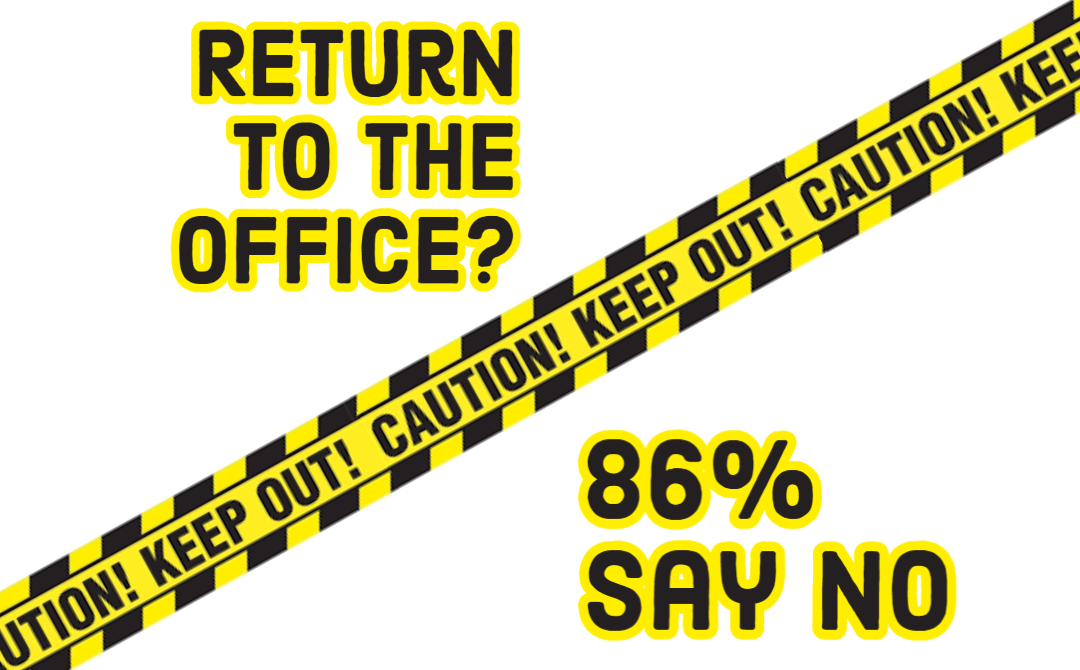

86% of people working from home in the US, Canada, and the UK don’t think it’s time to head back, according to a new survey.

The coronavirus pandemic has officially transformed the workplace, as many governments and companies shifted employees to working from home during the global health crisis. According to a recent survey by Gartner, more than half of organisations surveyed said that at least 81% of their employees are working remotely during COVID-19—and even after the crisis subsides, working from home may be here to stay.

Still, the economic toll of the pandemic, and its disruptions to daily life, are causing many to consider how—and when––companies can bring employees back to the office. President Trump, for instance, recently tweeted that he is focusing on “getting America back to work.”

Still, the uncertainty of the situation and the broad lack of testing are cause for concern for many workers. During a phone call with Trump, a group of business executives told the president that more testing was required before Americans “would be confident enough to return to work, eat at restaurants or shop in retail establishments.”

A whopping 86% of workers say it’s too soon to go back to the office, according to a new survey by O.C. Tanner of 1,581 employees in the US, Canada, and the UK.

“As part of our survey, we asked employees why it was too early to return to work,” said Alexander Lovell, director of research and assessment at O.C. Tanner. “The most common answer? ‘People are still getting sick.’ The virus is still spreading, and employees are monitoring these developments closely. They point to the evidence that people can be asymptomatic and continue to spread the virus. As one employee related, ‘What if I killed my 58-year-old co-worker? I might have it and simply not know.'”

As for when, exactly, workers should consider returning to work, the survey, taken April 19 and 20, shows:

4% — this week

5% — next week

19% — in 2-4 weeks

26% — in one month

34% — 2-3 months from now

13% — longer than three months from now

Some employees did not believe that it was too soon to return to work. Workers who did not live alone—they had a spouse, partner, or roommate—were three times more likely to fall in this category, suggesting that working from home with others might take a deeper toll or impact productivity.

Additionally, employees with school-age children who must now be taught from home were two and a half times more likely to fall in the camp of thinking it was not too soon to consider going back to work, according to the study. This also suggested that the office environment might be a welcome relief from a new life of working and home-schooling.

Source: Techrepublic.com

Apr 27, 2020 | HR, Management

The fourth COVID-19 Pulse Survey also revealed that 77% of US CFOs are planning to change workplace safety measures and that 2020 is a “lost year.”

Some 32% of US chief financial officers are anticipating layoffs in the next six months—up from 26% two weeks ago—and 49% are planning to make remote work a permanent option for roles that allow it, according to PwC’s fourth COVID-19 Pulse Survey released Monday.

Layoffs in traditional manufacturing are expected to be higher and lower in financial services, where roles tend to lend themselves to remote work, PwC officials said during a noontime conference call to discuss the latest survey results.

Additional findings are that 77% of US CFOs anticipate changing workplace safety measures upon returning to on-site work, as employers focus on protecting employees, 65% anticipate reconfiguring work sites to promote physical distancing, and 52% anticipate changing and/or alternating shifts to reduce exposure, the survey found.

In talks with dozens of CFOs in the past couple of weeks, foremost on their minds is not just the question of how to get people safely back to physical offices but “what does work look like going forward,” in light of the fact that remote work is proving effective, said PwC Chair Tim Ryan. Other questions Ryan said he’s hearing are about how companies should be managing costs and productivity needs.

But consistently, the “main theme” is about employee safety, he said.

“Virtually every company we speak with is putting the health and well-being of employees as a top priority and as they think about coming back to work, that’s first and foremost on their minds,” Ryan added.

“Lost year”

Over 300 CFOs responded to the most recent survey, which PwC conducts every two weeks, the firm said. The key themes where responses have changed between this survey and the last one reveal differences from a sector perspective, said Amity Millhiser, PwC’s chief clients officer. The biggest sentiments are around businesses returning to the workplace and the effect on the workforce, especially in furloughs and layoffs and impact on revenue and earnings, Millhiser said.

On the return to the workplace, 65% of CFOs said their companies will reconfigure worksites to promote physical distance, and “companies will increasingly look to digital solutions to adapt to physical distancing,” she said.

Some will do some contact tracing and there will be a greater emphasis on “that kind of technology” as opposed to manual workarounds as technology becomes available and the new normal for how companies work in offices, Millhiser said.

Workforce health and safety will also become “a critical job benefit” and more technologies will be leveraged in traditional offices and increasing remote workforces, she added.

As they were two weeks ago, CFOs remain pretty evenly split on how long it will be to get “back to normal,” Millhiser said.

Protecting cash and liquidity positions is paramount for CFOs, the survey found. “Financial impacts of COVID-19, including effects on liquidity and capital resources, remain the top concern of CFOs (71%). Over half (56%) say they are changing company financing plans, up from 46% two weeks ago,” the survey said.

Approaches they’re taking include hiring freezes and tightening controls on discretionary costs, such as ending travel and the use of contractors, according to the survey. At the same time, investments are being made in areas that are considered important to companies’ future growth, including digital transformation, customer experience, and cybersecurity and privacy initiatives, the survey said.

More than half (53%) said they are projecting losses to be greater than 10% this year. While experiences and changes differ by sector, the combination of the increased negative impact on earnings and revenue and the longer time to come back to normal is leading many CFOs to conclude that 2020 is “a lost year for them,” Millhiser said.

As states start to lift stay-at-home orders and reopen local economies, 52% of CFO respondents said their businesses could return to normal in less than three months if COVID-19 were to end immediately, the survey said.

New insight from survey data shows that less than a quarter of respondents (22%) indicate they plan to implement contact tracing as part of their plan to reopen their workplaces.

PwC also announced it has created a Check-In with Automatic Contact Tracing tool that allows companies to help quickly identify and alert employees who may have come into contact with a co-worker who has tested positive for COVID-19.

Additional survey results

The top concern of CFOs:

71% of respondents indicate that financial impacts remain a top concern.

Revenue:

80% of respondents expect that COVID-19 will decrease their company’s revenue and/or profits this year.

12% of respondents report that COVID-19’s impact on revenue and/or profits is still too difficult to assess at present.

5% of respondents expect a decrease in revenue of over 50%.

Financial actions:

86% are considering implementing cost containment (up 4 percentage points).

70% are considering deferring or canceling planned investments. Of these respondents, 80% are considering delaying or canceling facilities/general CapEx, 62% considering workforce, and 48% considering IT.

40% of CFOs are indicating no change to their strategies (up 6 percentage points) while 15% indicated an increased appetite for M&A.

91% plan to include a discussion of COVID-19 in upcoming external reporting.

50% plan to include discussion around COVID-19 in financial statements.

Supply chains:

56% are planning to develop additional, alternate sourcing options for their supply chains.

54% are planning to understand the financial and operational health of their suppliers.

“We are seeing many geographies being considered [for additional sourcing], not just domestically—and frankly, there’s a lot of excitement about that,” Ryan said. Stressing that “there’s a long tail” with adding additional suppliers, he said areas besides the US that can expect to see an uptick in sourcing include Vietnam and Malaysia, as well as Mexico and Canada.

“If you were to unplug with China completely, it’s a firehose,” Ryan added. “You’ll see many geographies benefit, all in the name of diversification.”

Source: TechRepublic.com

Apr 24, 2020 | HR, Management

Whether due to budget cuts or performance, letting staff go is sometimes a necessity, even during a pandemic. Here’s how to best handle the sensitive situation.

The coronavirus pandemic has sent shock waves through the enterprise forcing companies to make tough employment decisions with their staff. While the virus has directly resulted in layoffs and furloughs, some companies may have needed to terminate employee contracts before the disease’s outbreak, putting them in a particularly difficult position given the current economic climate.

Those who have been laid off or furloughed are flocking to apply for unemployment benefits: More than 26 million unemployment claims have been made since the start of the coronavirus-related shutdowns, so supervisors that are considering letting an employee go need to think long and hard about the timing, experts say.

“[Companies and HR professionals] should consider whether the reason is one for which they would have terminated the employee had we not been in this COVID-19 environment,” said Kelly Charles-Collins, unconscious bias expert at HR Legally Speaking.

“Tensions are high and patience is low. Perhaps things that an employee would not have been terminated for if we were in our regular workplaces may trigger a different reaction in this remote working environment,” Charles-Collins said.

However, companies also shouldn’t feel guilty if they ultimately decide to let someone go, said Neal Taparia, co-founder of SOTA Partners.

“It’s very easy to feel bad about it, but at the end of the day, you’re running a business, and other people are dependent on you,” Taparia said. “It’s a situation where you have to think about the greater good and be financially disciplined about it.”

Terminating an employee during the coronavirus pandemic is undoubtedly delicate, as the disease has impacted people mentally and economically. HR managers and supervisors may also have difficulty letting remote employees go, as remote work could be a new way of work for the company.

How to terminate an employee during COVID-19

The following steps and considerations can help HR managers appropriately navigate employment termination during the unprecedented time of COVID-19.

Maintain transparency

If you think your company might need to make layoffs, Taparia said to be open about that from the start.

“We’ve been trying to be as transparent and communicative as possible about what’s going on.” Taparia said. “This also means trying to be more transparent on how we’re trying to plan our company out financially.

“We’ve explained to them that there’s certain milestones that we need to hit, and within different periods of time we’ll continually evaluate the business,” Taparia said. “Not being transparent is even worse because they’re left into this world of uncertainty.”

Consider making the termination discussion impromptu

Notifying the company layoffs or terminations may be coming is important, but the actual conversation shouldn’t necessarily be expected, according to Taparia.

Taparia has run a few businesses. During an employment termination at one of his businesses, Taparia said there was an incident with the employee having known the difficult conversation was coming.

“In one instance, this employee became suspicious [of termination] because our HR lead was going to be in the meeting with myself,” Taparia said. “After we had that hard conversation, terminated the employee, and cut off access to email, when we looked through the email, the employee had sent himself a bunch of proprietary files from our company.

Upon suspecting the meeting was coming, the employee sent I private business information. Ever since that incident, Taparia said they have kept termination meetings as impromptu as possible, for the sake of security.

“It’s a ‘Hey, I need to talk to you,’ situation,” Taparia said. “Try not to mention that an HR professional will be in the meeting. That tends to be a surprise. But to me, that surprise is well worth it to prevent any type of IP loss.”

Have the conversation face-to-face

These conversations are ideally done in person, but a remote work environment doesn’t allow for that capability. HR managers should do the next best thing and have the conversation face-to-face over video, Charles-Collins said.

“We have access to technology that makes these types of face-to-face” meetings possible. Make sure that the meeting is not broadcast to anyone that should not have access,” Charles-Collins said. “If they are using technology like Zoom, they can require a password.

“Conduct the meeting just as if they would if they were in the office,” Charles-Collins said. “If they would not regularly record the meeting, I would recommend not doing so or allowing the employee to do so. This will require disabling the recording feature. Make the meeting short and respectful.”

Take care of the employee

Employment termination is a devastating blow in any scenario, but can be especially harmful during a worldwide crisis.

“Terminating an employee is never easy, but it should be humane,” Charles-Collins said. “Someone is losing their livelihood and people are not their best behavior. So, while their misconduct may be against company policy or even in violation of the law, our humanity should not be discounted or disregarded.”

To help during this time, Taparia said he offers to act as a reference for the terminated employee, whether it be via phone or recommendation letter. He said he has also pointed terminated workers toward platforms such as Upwork or Textbroker for easy contract jobs.

“We do give some small severance,” Taparia said. “We want to do what we can so they land on their feet. I even told them that I would try to think of contracting jobs, too, to help them in the meantime.”

“You have to go above and beyond to think about how you can take care of your employees. It’s not a ‘cut the cord and forget it’ situation, which some companies normally do during general business times,” Taparia said. “In my experience, you want to look after people.”

Postpone exit interviews

Exit interviews are a critical step for companies in the employment termination process, however, Taparia recommended letting the employee settle down first. He said that is what his company recently did with a former employee.

“The reason we decided not to [immediately have the interview] was it just felt awkward doing it, given all the circumstances, and we didn’t want this person to continue to feel anxiety around everything going on,” Taparia said.

“We plan on, in the next month or two, touching base with this employee every single week to see how it’s going. When things have cooled down, I’d like to send them a survey on what they think we could do better,” Taparia said. “[This would] give us some authentic feedback, as opposed to feedback that’s very emotionally driven, because everything happened so sudden.”

Source: TechRepublic.com

Apr 24, 2020 | HR, Management

If an employee decides to pursue another job during the coronavirus pandemic, organizations must be prepared to keep proprietary data and company technology safe.

With COVID-19 shaking up employment, many teams are facing furloughs and layoffs. Some employees, however, are also opting to leave their jobs during this chaotic time. No matter the reason, companies must have the proper plans and security in place for an employee’s departure.

Companies have been forced to quickly adapt to remote work because of the coronavirus, many of which have never worked entirely remotely previously.

“Organizations are frantically trying to enable existing workforces to become full-time remote workforces,” said Arun Kothanath, chief security strategist at Clango, an identity and access management (IAM) consultancy. “This requires organizations to rapidly roll out VPNs and authentication technologies, such as multi-factor authentication, while enabling employees to be able to connect to mission-critical assets from their remote workstations.”

While equipping employees with secure connections is one of the crucial first steps to launching a remote workforce, businesses must also consider how to rescind such access upon employee termination or departure.

“The only way to secure critical business data is to control the access to it,” Kothanath said. “When an employee is terminated or informs the organization they are leaving for another company, there must be a way for an IT manager to immediately revoke the employee’s access.”

Neal Taparia, co-founder of SOTA Partners, said he once experienced an employee send themselves sensitive business information upon figuring out their employment would be terminated.

To help prevent other organizations from facing similar situations, Taparia and other experts outlined the following best practices for keeping company information and hardware secure in the event of an employee leaving.

IT’s responsibility for when an employee departs the company

Remove email access

After Taparia’s bad experience, he said the first thing his company does is shut off access to the employee’s email, that way the employee can’t send themselves items.

“We’ll also quickly peruse the type of activity they’ve had in their Google accounts. We use the Google Apps Productivity Suite, and it gives you some administrative abilities to see what’s going on,” Taparia said.

“We’ll look for any type of suspicious behavior, and we’ll try not to signal to [employee] that we’re going to have this tough conversation so they have time to [transmit sensitive files],” he added.

Confiscate company hardware

One problem employers might run into is how to retrieve company hardware from its remote workers.

Taparia said companies should make this process easy. His organization provides a box with a shipping label for the worker to send their items. He also said to guarantee the employee sends hardware back, his organization leverages severance.

“We try to get them a box with a shipping label as fast as possible, and we’ll tell them, ‘We want to give you the severance, but we do need that equipment back as soon as possible. If you want full severance, we need that back ASAP, and we’re going to make it as easy for you as it is possible to put it in the box and put the shipping label on it and just get it back to us,'” Taparia said.

Return in-office items

Since many companies were forced into remote work with COVID-19, employees may still have belongings in the office they need upon termination or departure.

“We told the employee we let go that we’d return their personal items via Fedex when we deemed it safe to return to the office again,” Taparia said.

“If it’s urgent, I still wouldn’t recommend compromising any of your staff to go to the office to return personal items. Right now, risking your health is outside of anyone’s responsibilities,” Taparia added.

Eliminate all digital accounts

The last component to consider is the employee’s various digital accounts. Just because they leave your organization, that doesn’t mean they may not try to access various accounts from personal devices.

“You need to consider all the digital assets they have remote access to as well,” said Finn Faldi, president at TeamViewer Americas, an enterprise remote access and support provider.

“Single-sign on and conditional access tools can provide you with one of the most secure environments to help you manage who gets access to what digital assets,” Faldi said. “If you have these tools in place as part of your remote connectivity solution, you can turn off all access to all company systems in real time as individual employees are off-boarded.”

Additionally, organizations that have an IAM program in place can easily revoke employee access to critical business data and assets, from anywhere, Kothanath added.

Source: TechRepublic.com

Recent Comments